" transform="translate(9 6)" width="6px"/></svg>)

Housing Tax Reform Won’t Remove Pressure: It Will Reshape It

The 2026 Federal Budget has now confirmed some of the most significant housing tax reforms Australia has seen in decades. Instead of solving affordability issues, they will most likely shift…

The 2026 Federal Budget has now confirmed some of the most significant housing tax reforms Australia has seen in decades.

From 1 July 2027:

– Negative gearing for residential property will largely be restricted to newly built homes;

– The current 50% capital gains tax (CGT) discount will be replaced with an inflation-based indexation system alongside a proposed 30% minimum tax on capital gains; and

– Discretionary trusts will face a proposed 30% minimum tax from 1 July 2028.

The intent behind these reforms is fairly straightforward: reduce investor demand, improve affordability for first-home buyers, and slow down house price growth.

And to be fair, there is logic behind that thinking. Tax settings do influence investor behaviour to some extent, and few serious economists would argue otherwise.

But Australia’s housing challenges are more complicated than simply “fewer investors equals more affordable housing”.

Even if tax reform changes demand for certain asset types, it does not remove the underlying demand for housing. Most likely, it would simply shift housing pressure from one market to another within the system. At the same time, a shift in demand wouldn’t fix the supply issues that are contributing heavily to the affordability crisis.

In many ways, these reforms just reshape the housing market more than they solve it.

We’ll break it down in this blog.

What The Government Is Trying To Achieve

The argument for changing negative gearing or the CGT discount is that investors currently have advantages that owner-occupiers don’t.

If property investment becomes less tax-effective, investor demand may slow. In theory, it could reduce competition and make it easier for first-home buyers to enter the market.

That is the core policy objective, and honestly, I can understand why the idea resonates politically. Housing affordability has become a genuine issue across Australia, especially in the east coast cities.

But the public conversation sometimes oversimplifies where the pressure is actually from.

Australia’s Housing Problem Is More Structural Than Tax-Driven

Australia’s affordability pressures are fundamentally driven by a mismatch between limited housing supply and fast-growing demand.

Over the past 5-10 years, we have had:

reduced stock mobility due to high transaction costs;

rising construction costs;

labour shortages;

slow land release;

approval delays;

infrastructure bottlenecks; and

consequently, not enough new housing being delivered fast enough.

At the same time, demand has continued growing – high migration has been driving strong population growth.

As a result, stock for sale and for lease have both declined significantly compared to pre-COVID levels:

The national total number of for-sale listings is now more than 30% lower than in 2019.

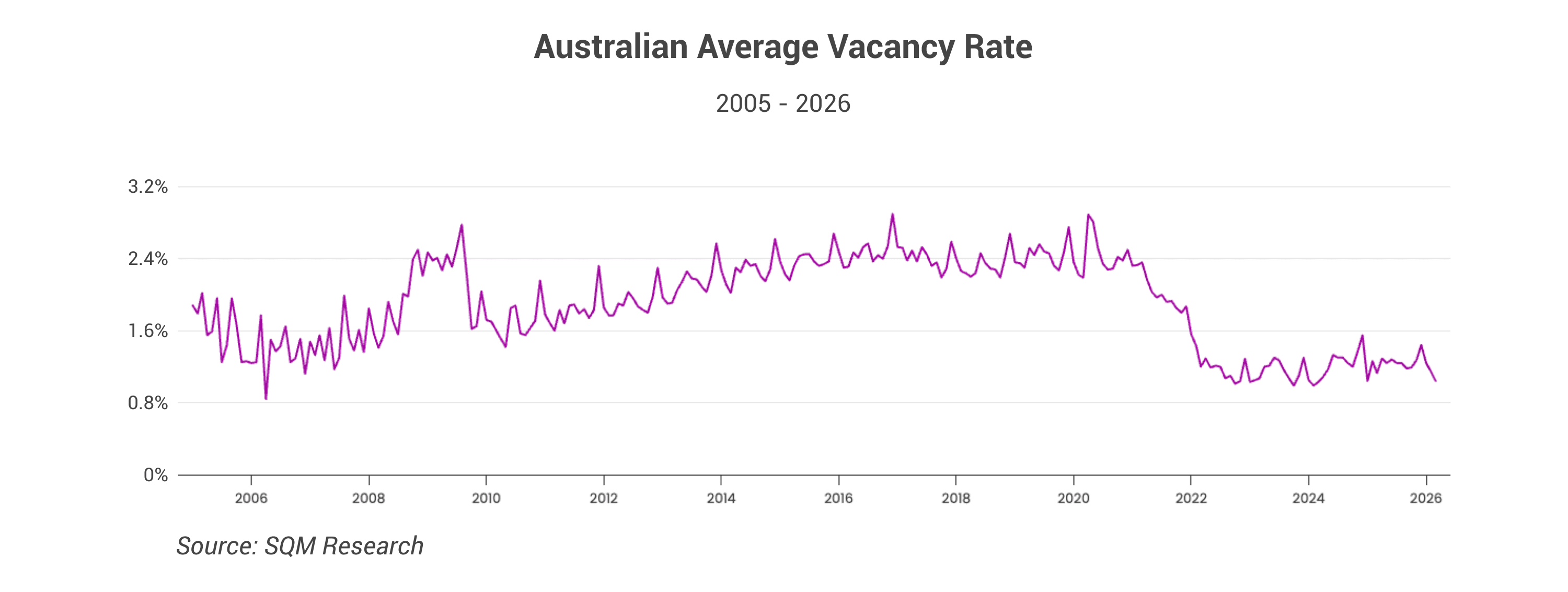

The national average rental vacancy rate has dropped from 2.5% in 2019 to the 1.0%.

As long as the supply-demand imbalance exists, housing market pressure and price growth will persist. Tax settings may influence demand at the margins, but they do not suddenly reduce population growth, stop migration, or create a large amount of new housing supply.

That’s where I struggle to see how tax reform can solve affordability problems.

Housing Demand Will Redestribute, But Not Disappear

Even if tax reform reduces investor participation, especially in the established housing market, housing demand does not disappear.

A more realistic outcome is that:

– some owner-occupier demand replaces investor demand;

– some renters transition into ownership;

– while many other households continue competing in the rental market.

Because the renter-to-owner-occupier transition is unlikely to be a simple one-to-one shift.

Many renters are not financially ready to buy immediately, especially in expensive cities like Sydney, Melbourne, Brisbane, etc.

In reality, it is probably higher-income renters or those with stronger equity positions who will transition most smoothly into ownership.

At the same time:

– a significant renter population will still rely on rental housing;

– rental demand would continue being driven by job opportunities, amenities and lifestyle preferences rather than simply where rental supply is available;

– rental supply may potentially shrink faster than the renter pool itself.

If that happens:

– competition in the rental market, especially in the more established areas, could intensify;

– rental affordability could worsen; and

– housing pressure would simply shift from purchase prices to rents.

Improving ownership access for some households does not necessarily mean housing becomes more affordable across the entire system.

Taking My Own Situation As An Example

My partner and I rent in Potts Point, which is one of Sydney’s more established and tightly held inner-city suburbs.

Realistically, even if our landlord sold the apartment tomorrow, we probably wouldn’t buy the property ourselves.

Partly because buying an apartment in Potts Point does not align with our current investment goals, and partly because purchasing a house in this part of Sydney that meets our lifestyle needs is far beyond our financial reach at this stage.

If it’s not sold to another investor, the buyer would most likely be:

a higher-income couple;

a downsizer; or

someone with a much stronger equity position (eg. family-assisted FHB)

But we would still need somewhere to live.

That could mean:

– competing harder for another rental in the same area, paying higher rents; or

– moving farther from the CBD, compromising on convenience and lifestyle; or

– eventually purchasing in a much more affordable but less convenient suburb farther away.

Many households would likely go through similar adjustments.

Housing demand does not disappear.

It shifts:

– geographically;

– between ownership and rental markets; and

– across different price points.

From my perspective as a renter, affordability wouldn’t necessarily improve just because there are fewer investors. In fact, the pressure could become even greater, through higher rents, longer commutes, or compromises on lifestyle and convenience.

Tax Reform Will Reshape Investor Behaviour

One important thing to keep in mind is that markets rarely remain static after major policy changes.

Whilst tax reform does not fundamentally solve affordability issues, it can still significantly reshape investor behaviour across the property market.

Negative gearing reform may drive demand toward higher cash flow

Now that negative gearing is limited to new builds (for any property purchased after 12th May 2026), investors will likely become far more selective about where and how they allocate capital.

Instead of simply exiting the market altogether, many investors may adapt by prioritising:

Stronger cashflow asset types;

higher-yield markets;

more affordable price points; or

new builds, where tax incentives remain more favourable.

That shift may become particularly noticeable in higher-price, lower-yield markets, where cash flow is already under pressure.

The CGT discount reform may have more complicated effects on investor behaviour

A lot of the public discussion has framed the reform as “investors losing the 50% discount.”

But the shift toward inflation-based indexation is actually cleaner than a blunt 50% discount.

Under the current system, once an asset is held for more than 12 months, investors automatically receive a flat 50% discount on nominal gains.

That treats:

– inflation-driven gains,

– speculative short-term gains, and

– genuine long-term real gains,

in largely the same way.

The new indexation approach is arguably more economically coherent because it focuses more on taxing real gains rather than inflation-driven nominal gains.

It also removes the sharp 12-month behavioural threshold that can encourage relatively short-term speculative investing.

In fact, under the indexation system, investors are encouraged to be more rational and focus on:

– long-term fundamentals;

– a balance between real capital growth and cash flow;

– opportunity cost; and

– strategic portfolio allocation,

rather than purely maximising tax concessions.

However, the shift toward indexation may still create some lock-in effects behaviourally.

While indexation merely adjusts for inflation rather than providing an increasing concession over time, some investors may still perceive a larger future tax benefit from holding assets longer, potentially influencing exiting decisions to some extent.

How Markets Historically Adapted to Policy Changes

We have already seen how markets adapt to tax reforms and policy changes, both domestically and overseas.

Incentives for New Builds

One possible reform to negative gearing is to restrict it to new builds. Australia has experienced how markets reacted to new-build-specific incentives during the HomeBuilder period (2020-2021).

HomeBuilder successfully stimulated construction demand, but it also coincided with rising construction costs, labour shortages, project delays, and significant pressure on builders as industry capacity struggled to keep up.

It was a reminder that stimulating demand is one thing, expanding supply capacity fast enough is another.

That is something many people underestimate.

If governments heavily incentivise new construction again while the industry is already dealing with labour shortages, material constraints, builder collapses, and feasibility pressure, the market response may become more complicated than expected.

Negative Gearing Reforms

In New Zealand, the government phased out mortgage interest deductibility for many investment properties from 2021 to 2025, while maintaining incentives for new builds. In the UK, Section 24 reforms, gradually phased in from 2017 to 2020, reduced the tax effectiveness of leveraged property investing for landlords.

In both cases:

investor demand became relatively more cautious;

investors became more cash-flow focused;

some investors shifted toward higher-yield markets;

some investment properties were sold; and

rental market dynamics evolved.

But neither country solved housing affordability with just that tax reform.

That is partly because housing systems are influenced by many more forces than tax policy alone, especially in markets already facing supply constraints.

What Investors Should Actually Focus On

History has shown that when policy changes, the market does not stop functioning, but rather adapts.

For investors, the risk lies in becoming overly focused on political headlines while overlooking the broader fundamentals that continue to drive Australia’s housing market.

While tax policy matters, over the long term, housing performance is still heavily influenced by:

land scarcity;

population growth;

infrastructure investment;

employment growth;

wage growth;

construction pipelines;

etc.

Markets with persistent housing shortages will not suddenly lose pressure simply because tax settings change.

If anything:

– some rental markets may tighten further if investment slows, while demand increases remain strong;

– while some affordable or higher-yield markets may become increasingly attractive as investors become more cash-flow-sensitive.

The important thing to understand is that tax reform does not remove housing pressure from the system.

More likely, it redistributes incentives and reshapes where that pressure appears.

As the legislation develops further, the details, and therefore the market implications, may continue evolving as well. Over the coming weeks, we’ll continue breaking down how the tax reforms are likely to affect the Australian property market and participants’ behaviours – Stay tuned!

At InvestorKit, we believe property investing decisions should be driven by clarity, long-term fundamentals, and strategic thinking rather than political headlines or emotions.

If you would like clarity around your next property purchase in this changing environment, feel free to book a free discovery call with our team.

Keep Reading

" transform="translate(5 5)" width="14px"/></svg>)