" transform="translate(9 6)" width="6px"/></svg>)

The Danger of Making Property Decisions Based on Today’s Interest Rates

Should you wait for interest rates to fall before investing? Discover why long-term property investors should focus on market fundamentals, not today's borrowing costs, when making investment decisions.

High interest rates have caused many investors to delay purchasing property, waiting for borrowing conditions to improve before entering the market.

While this may seem like a prudent approach, it’s worth remembering that interest rates are only one snapshot in time. Property investment is a long-term strategy, whereas interest rates are a short-term monetary policy tool that moves through economic cycles.

Understanding this distinction can help investors avoid making long-term decisions based on temporary market conditions.

Today’s Interest Rates Are Not a Permanent Reality

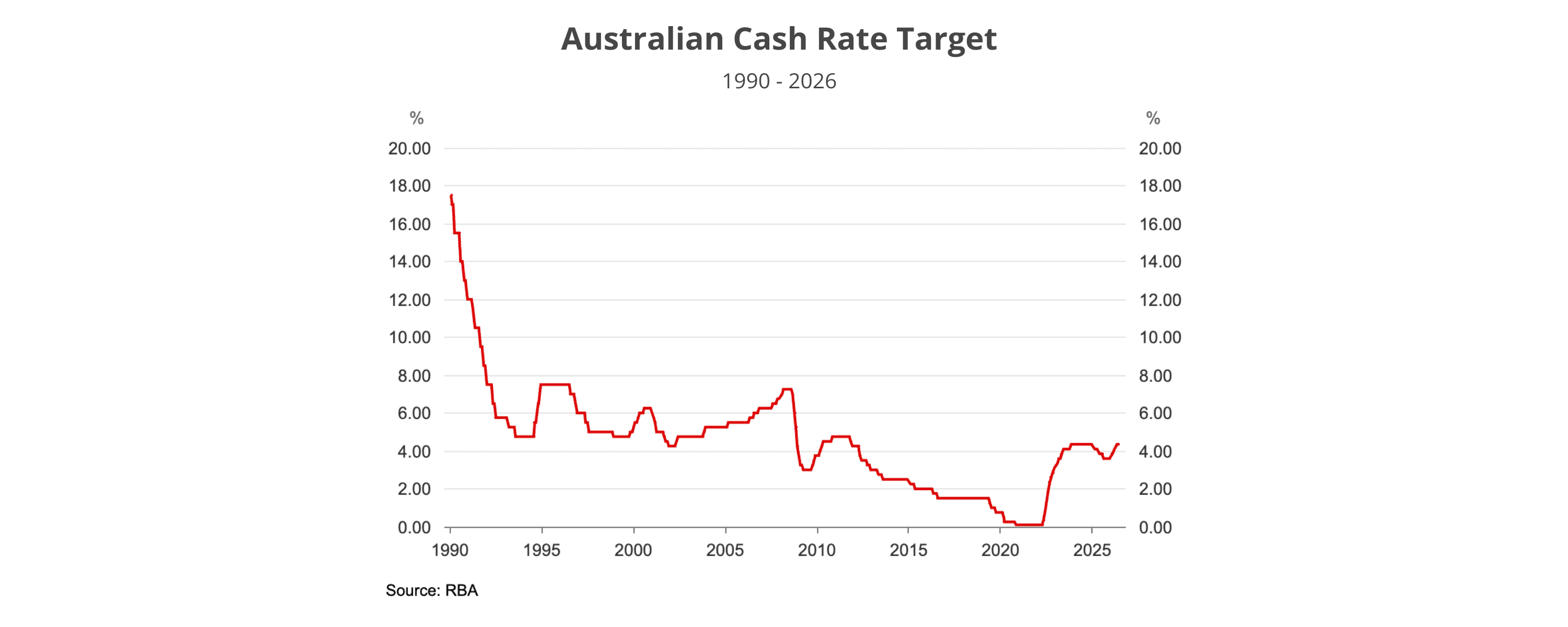

Australia’s cash rate is currently at its highest level in more than a decade, resulting in higher mortgage repayments and reduced borrowing capacity.

While today’s borrowing conditions feel restrictive, they should not necessarily be viewed as permanent.

The Reserve Bank adjusts interest rates to achieve its inflation target while supporting broader economic stability. When inflation rises above the target range, higher interest rates help slow demand and reduce inflationary pressure. If inflation returns sustainably towards the target range and economic conditions stabilise, maintaining highly restrictive interest rates would become less necessary.

For this reason, monetary policy has historically moved through periods of tightening and easing rather than remaining permanently high or permanently low (see chart below).

High interest rates have caused many investors to delay purchasing property, waiting for borrowing conditions to improve before entering the market.

While this may seem like a prudent approach, it’s worth remembering that interest rates are only one snapshot in time. Property investment is a long-term strategy, whereas interest rates are a short-term monetary policy tool that moves through economic cycles.

Understanding this distinction can help investors avoid making long-term decisions based on temporary market conditions.

Today’s Interest Rates Are Not a Permanent Reality

Australia’s cash rate is currently at its highest level in more than a decade, resulting in higher mortgage repayments and reduced borrowing capacity.

While today’s borrowing conditions feel restrictive, they should not necessarily be viewed as permanent.

The Reserve Bank adjusts interest rates to achieve its inflation target while supporting broader economic stability. When inflation rises above the target range, higher interest rates help slow demand and reduce inflationary pressure. If inflation returns sustainably towards the target range and economic conditions stabilise, maintaining highly restrictive interest rates would become less necessary.

For this reason, monetary policy has historically moved through periods of tightening and easing rather than remaining permanently high or permanently low (see chart below).

The table above shows how much a 2% rate drop can improve affordability across major cities. As borrowing capacity improves, more buyers may be able to compete for the same properties. Increased competition can put upward pressure on prices, meaning that by the time financing conditions feel more comfortable, purchasing a property could be more expensive.

In fact, price growth doesn’t perfectly correlate with interest rates. In the past 2 decades, we’ve seen multiple periods in which house prices continued to grow steadily when cash rates increased or remained high (see chart below).

Waiting for lower interest rates does not necessarily lead to a better investment outcome. In many cases, it simply means entering a more competitive market with higher prices.

Long-Term Market Fundamentals Continue to Support Property

While interest rates change over time, many of the structural drivers, or fundamentals, underpinning Australia’s housing market have remained remarkably consistent. Actually, strong fundamentals were why, in the previous chart, housing prices could continue to rise even in high- or rising-rate environments.

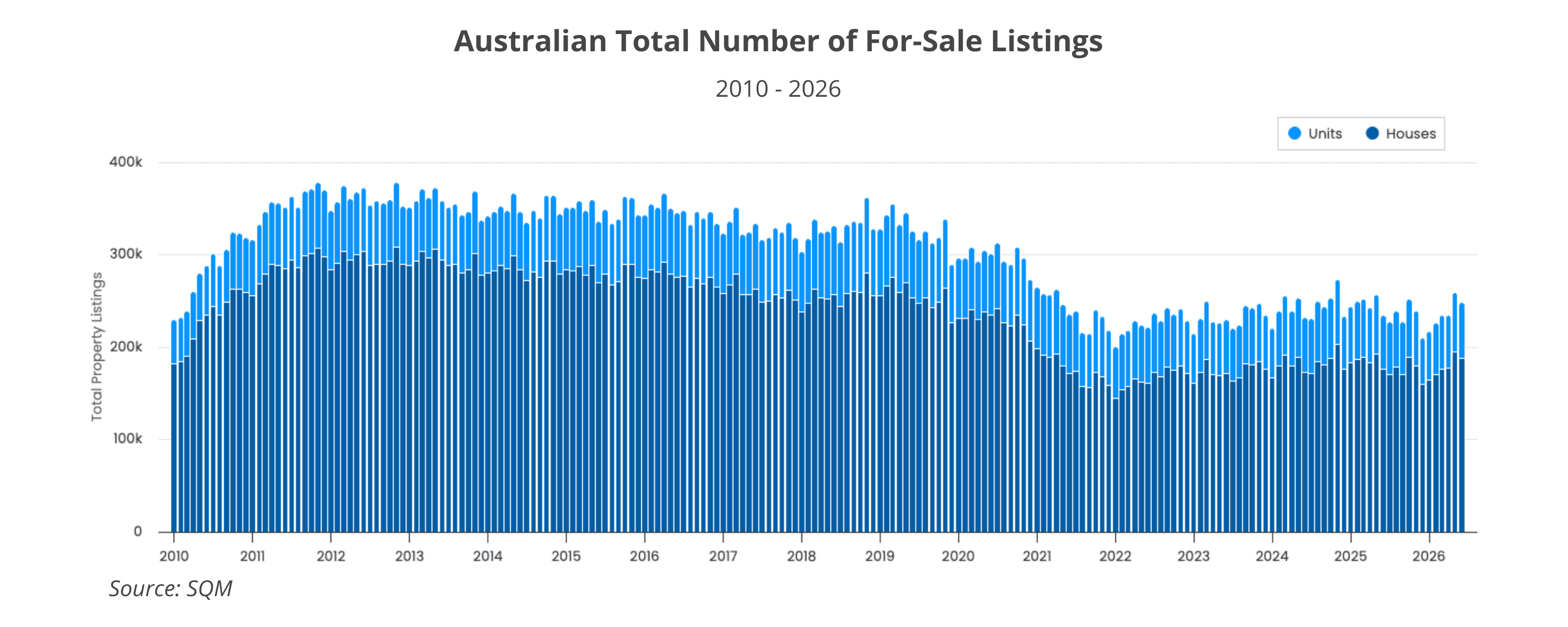

Looking at Australia’s housing fundamentals today, supply remains constrained across much of the country. Listing volumes are still well below pre-pandemic levels, rental vacancy rates remain historically low in many markets (see charts below), and strong population growth continues to drive additional housing demand.

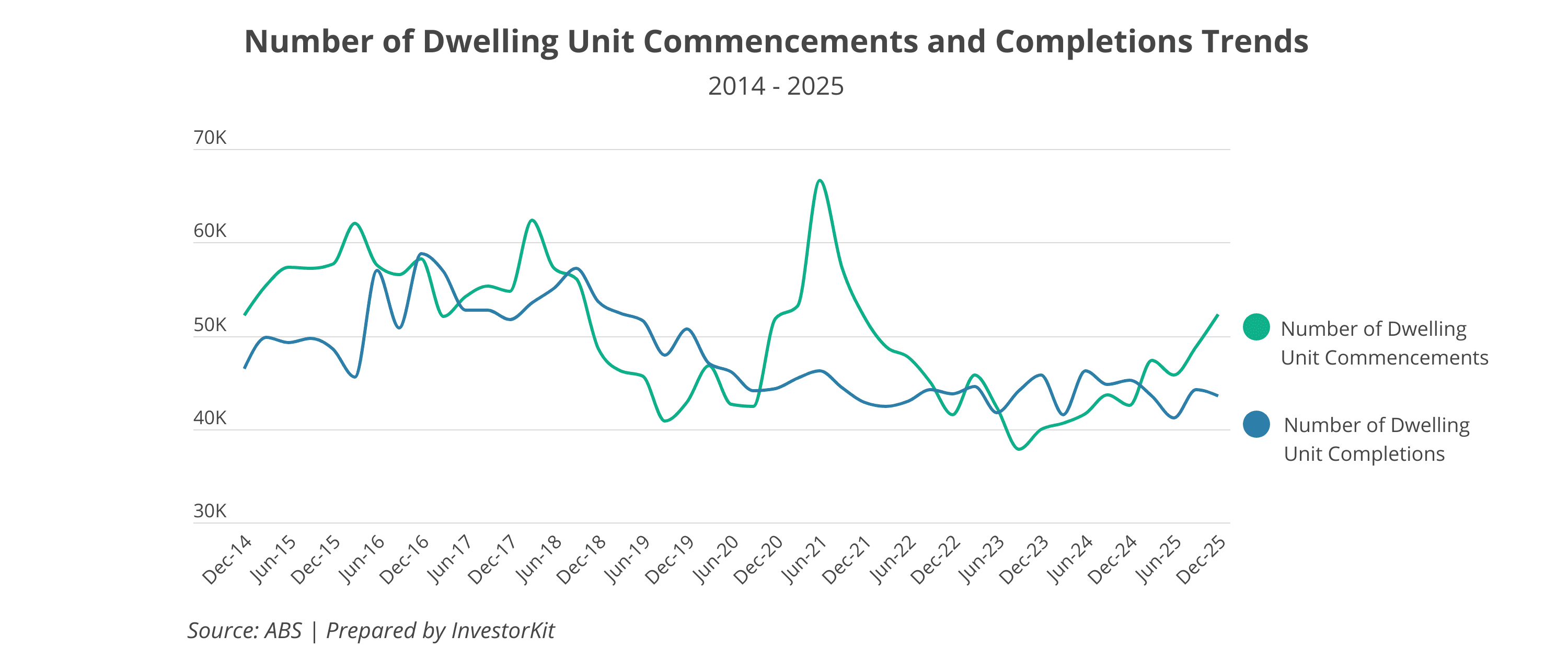

On the new supply side, although dwelling commencements have gradually recovered, housing completions remain well below the level required to meet Australia’s housing needs. High construction costs, labour shortages and capacity constraints across the building industry are likely to continue limiting new housing supply in the near term.

These structural factors tend to persist for many years, whereas interest rates can change over the course of just an economic cycle.

For long-term investors, the fundamental relationship between housing supply and demand is often more influential than today’s borrowing costs.

High Interest Rates Don’t Eliminate Investment Opportunities

High interest rates have undoubtedly reduced borrowing capacity and made some housing markets less affordable. In many locations, affordability constraints have softened buyer demand and moderated price growth.

However, Australia’s property market is far from homogeneous.

While some markets have become increasingly difficult to enter, others remain comparatively affordable and continue to attract demand. In many of these markets, housing supply remains constrained, rental demand is strong, and prices continue to grow rapidly despite the higher-interest-rate environment. The chart below shows some examples.

This highlights an important point: your decision is not whether to invest, but where to invest.

Property markets across Australia move through different stages of the cycle at different times. Some markets may be moving slowly due to affordability constraints, others continue to grow, or even accelerate, due to high housing demand and limited supply.

For investors, identifying these opportunities is often more important than perfectly timing changes in interest rates. Market selection has always been one of the most important drivers of investment performance, regardless of where interest rates sit.

Looking Beyond Today’s Interest Rates

Interest rates are an important consideration, but they should not become the sole factor driving a long-term property investment decision.

Monetary policy is cyclical. Borrowing capacity changes. Consumer confidence rises and falls. These are all moment-in-time metrics that help explain today’s market conditions, but they do not necessarily determine how property markets will perform over the coming years.

By comparison, structural drivers such as housing supply, population growth and local market fundamentals tend to persist over much longer periods and often have a greater influence on long-term market performance.

Most importantly, Australia’s property market is not one market. Different cities, regions and suburbs experience different conditions and move through different stages of the property cycle. While higher interest rates may limit opportunities in some locations, others continue to demonstrate strong fundamentals and healthy growth potential.

Rather than asking whether now is the right time to invest, investors may benefit more from asking where the strongest opportunities exist today.

At InvestorKit, our research focuses on identifying those opportunities by analysing market fundamentals across Australia. If you’d like to understand which markets continue to offer strong long-term investment potential in the current interest rate environment, book a FREE 15-minute Discovery Call with our team.

Keep Reading

" transform="translate(5 5)" width="14px"/></svg>)