" transform="translate(9 6)" width="6px"/></svg>)

Why Geopolitical Conflicts Rarely Move Australia’s Property Market?

When geopolitical tensions escalate, investors often ask the same question: What does it mean for property markets?

The recent escalation involving Iran, Israel and the United States has quickly captured global attention.

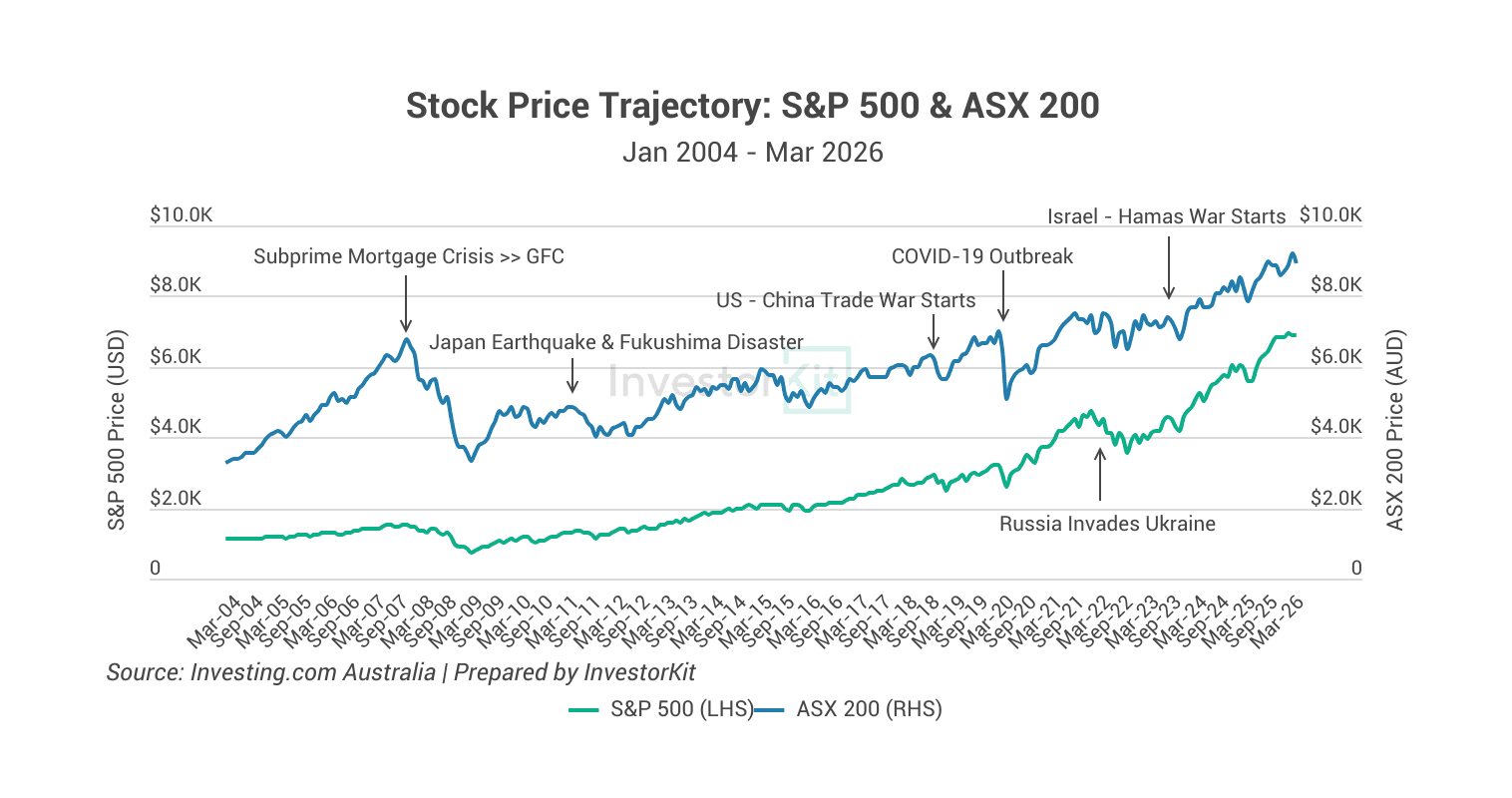

As tensions rose, financial markets reacted immediately. Oil prices briefly surged above US$119 per barrel on 9th Mar before falling back to under $90, and the Australian share market saw more than $100 billion wiped from its value that same day, before recovering gradually in the following days.

When geopolitical tensions escalate, investors often ask the same question:

What does it mean for property markets?

For Australia, the direct impact is usually very limited, whilst the indirect impact could be noticeable if the event lasts for a long time.

To understand it better, let’s look at how global events flow through the broader economy.

The Economic Transmission Channel

One of the most immediate effects of the current conflict has been on energy markets.

Disruptions to global oil supply can push prices higher, which then flows through to petrol prices and inflation.

In Australia, each US$1 increase in oil prices adds roughly one cent per litre to petrol prices. If oil prices were to stabilise around US$100 per barrel, that would represent a rise of around US$40-50 from earlier lows and could increase petrol prices by roughly 40–50 cents per litre (Shane Oliver, AMP).

Higher energy costs are like an increased tax on households and businesses, raising prices of goods and pushing up inflation. Households could have less disposable income left.

However, the above impact does not translate into immediate movements in housing markets.

Financial Markets React Immediately

Equity markets are highly liquid and globally integrated. Investors can buy or sell billions of dollars’ worth of shares within seconds, allowing prices to react immediately to new information.

Looking back over the past two decades, we see that almost every major event, whether it’s a natural disaster or a geopolitical conflict, has caused immediate disturbance in both the US and Australian share markets.

Property Markets Have Much Lower Liquidity

One reason geopolitical shocks rarely move housing markets is structural: property markets are far less liquid than financial markets.

Buying or selling property involves:

Weeks, if not months, of transaction time

significant transaction costs

financing approvals

etc.

These processes slow down market reactions. Unlike stocks, housing prices cannot adjust overnight in response to global news.

Another important factor is the nature of demand. Property is not purely a financial asset, but also a consumption good. Approximately two-thirds of property buyers are owner-occupiers purchasing homes to live in. While investors who may be responsive to market sentiment, homeowners rarely change their behaviour simply because geopolitical risks have increased.

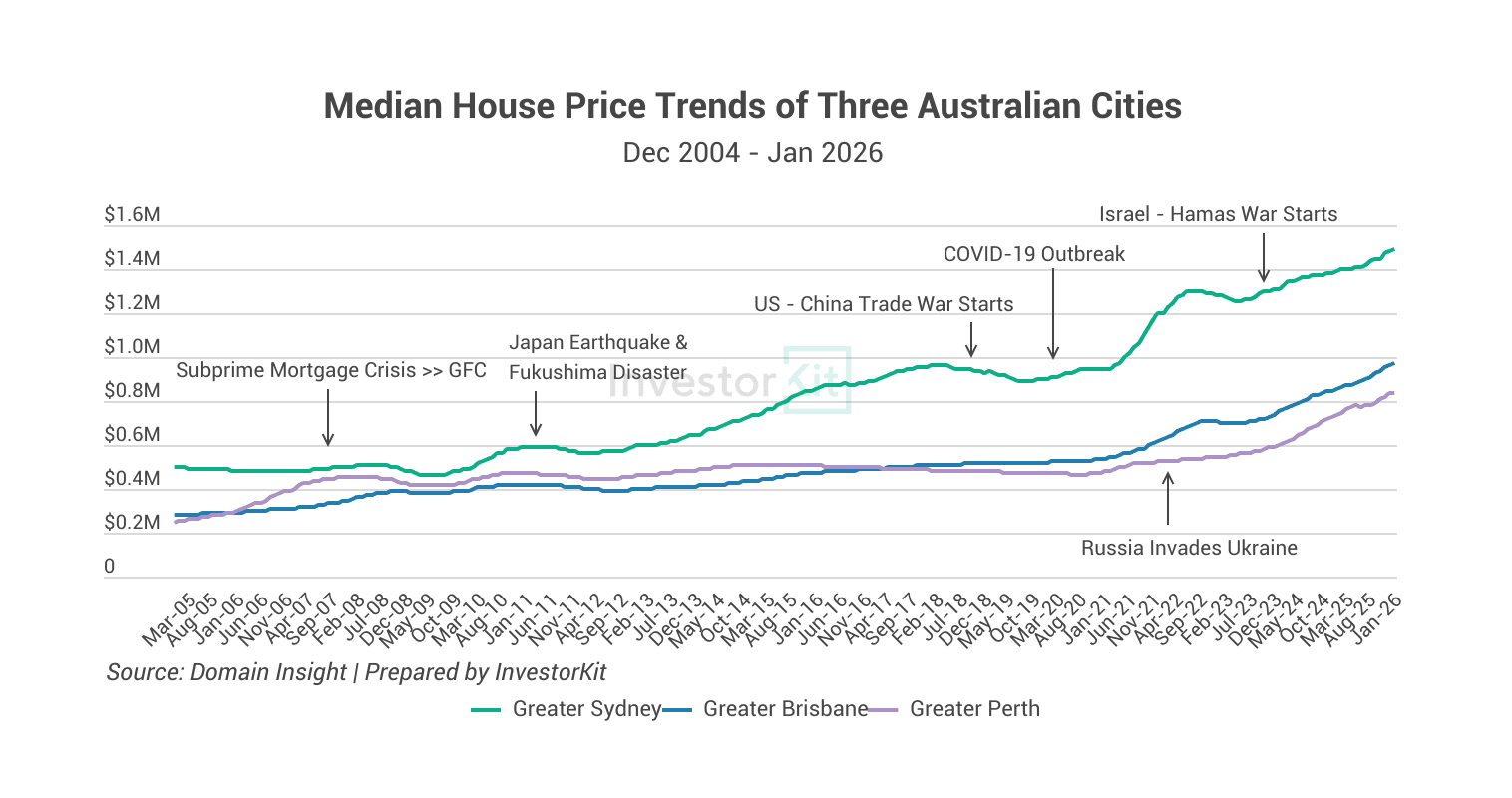

The chart below shows how unresponsive the Australian property prices have been to the same events mentioned above. We use 3 capital cities as representatives.

House prices didn’t decline until 2008, when the actual GFC took place.

Prices did decline after the Fukushima Disaster, but it’s more plausible that the decline was a cyclical correction after the post-GFC surge.

The US-China Trade War occurred during Sydney’s downfall. There is no evidence that the Trade War led to the price decline.

The rest of the events didn’t see any following price decline.

The Australian Property Market Is Primarily Driven by Local Factors

Australia’s housing market is also fundamentally localised.

The majority of property buyers in Australian cities are local households. Even the “global” cities such as Sydney, Melbourne and Brisbane are also largely driven by domestic demand and supply.

Demand for housing is closely linked to:

Population growth and migration

Local job market activity

Infrastructure services

Affordability relative to local incomes

Financial conditions (esp. borrowing capacity, and serviceability)

These factors tend not to respond significantly to geographic tensions, which contributes to the relative stability of housing markets compared with financial markets.

On top of that, housing supply shortage plays a structural role in driving the consistent growth of the Australian property market.

For many years, Australia has experienced persistent housing shortages due to factors such as:

Low stock mobility as a result of high transaction costs

Lack of land supply and slow planning processes

Slow construction pipelines

Strong population growth led by overseas migration

Shrinking household sizes

etc.

The supply shortage isn’t expected to be resolved in the near term. This structural dynamic often outweighs short-term global developments. Even during periods of international uncertainty, strong underlying demand and housing shortages can continue to support property prices, despite cyclical corrections here and there.

Interest Rates: The Real Impact

While geopolitical conflicts rarely move property markets directly, they can still influence housing indirectly, especially through interest rates.

Rising oil prices can push inflation higher. RBA has advised that the jump in oil prices could push inflation above the current forecast of 4.2% by June this year. An AMP estimate suggests that oil prices around US$100 per barrel could push Australian inflation to about 4.6%.

Higher inflation could mean that the RBA needs to keep interest rates higher for longer. Currently, all Big Four Banks are forecasting another 25 bps hike in the cash rate to 4.1%.

Interest rates are one of the most important drivers of housing cycles because they directly affect borrowing capacity. Higher rates reduce how much households can borrow and increase mortgage repayments, which tends to dampen housing demand. Lower rates, by contrast, expand borrowing capacity and often stimulate property markets.

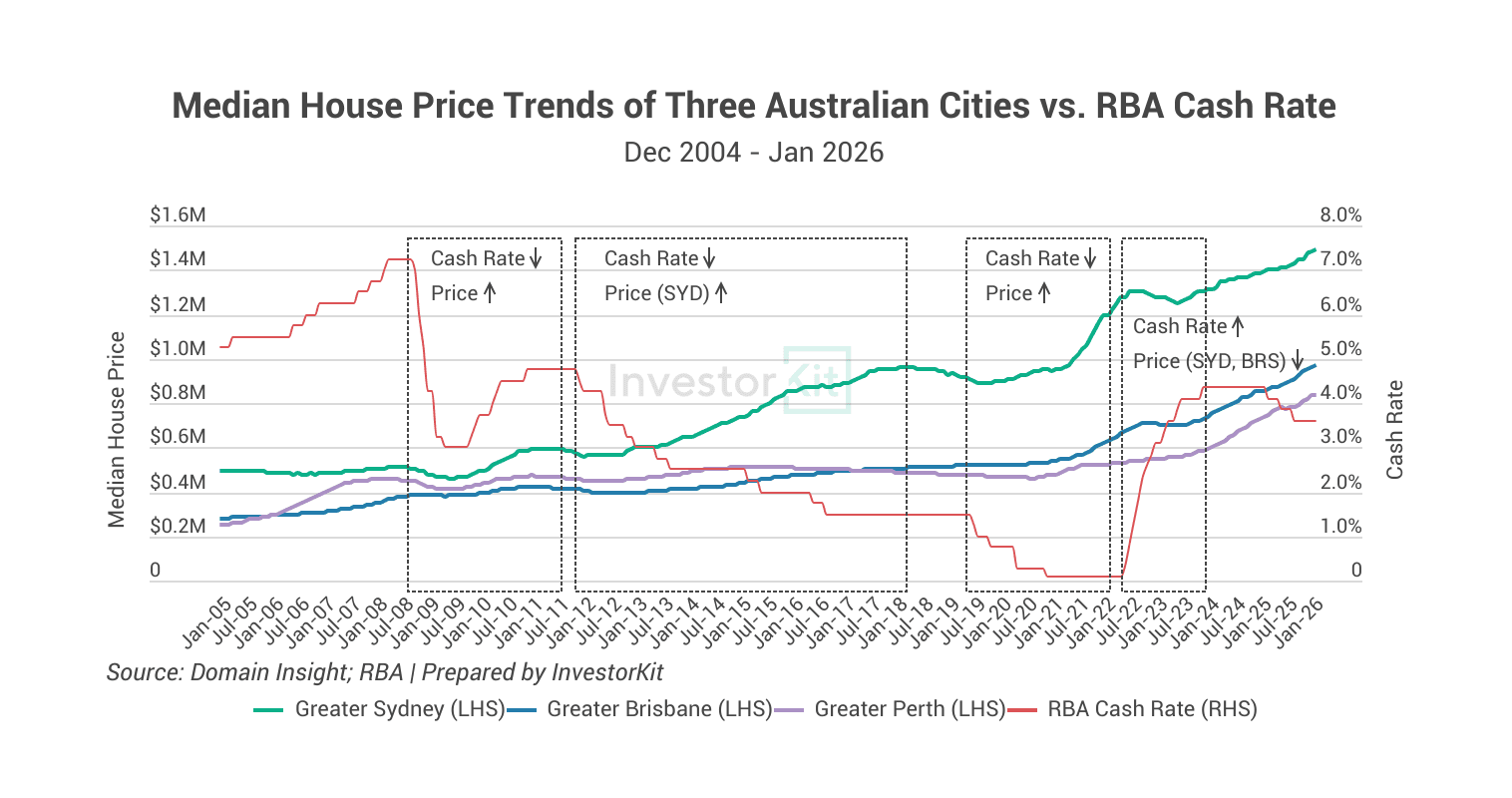

This is why property cycles in Australia historically align far more closely with interest rate movements than with geopolitical events (chart below).

That said, not all markets respond to interest rates the same way. In the chart above, Sydney is the most responsive, while Brisbane and Perth are much less so. This is another piece of evidence that property markets are influenced by many factors. Growth can be driven by different elements in different locations. An example is the boom in affordable markets since 2023, as we entered the high-rate environment.

Focus on the Fundamentals

While global conflicts can influence financial markets almost instantly, housing markets operate under very different dynamics. In practice, Australian property prices are driven far more by domestic fundamentals than by geopolitical headlines.

For Australian property investors, the most important indicators remain domestic fundamentals: population growth, migration trends, local economic development, local job market activity, interest rates, affordability, housing supply, government incentives, and more (For a full review of Australia’s housing fundamentals, check this whitepaper out: Australia’s Housing Fundamentals Analysis FY25/26). While geopolitical tensions may dominate global headlines, the forces shaping Australia’s housing market are much closer to home.

InvestorKit is a buyer’s agency focused on helping Australian property investors understand the market fundamentals and invest with clarity and long-term perspective, rather than being influenced by headlines. If you’re unsure about when to make your next move or where to invest, why not book a 15-minute free Discovery Call with our team to discuss your strategy?

Keep Reading

" transform="translate(5 5)" width="14px"/></svg>)