" transform="translate(9 6)" width="6px"/></svg>)

Greater Melbourne Property Market in 10 Charts

In this week’s blog, let’s dive into data and interpret Greater Melbourne’s house market pressure with 10 charts.

Melbourne: The newly named “Australia’s biggest city”.

As ABS updated the Melbourne Significant Urban Area (SUA)’s boundary to include Melton, Melbourne has officially become the most populous city in Australia. In this week’s Market Pressure Review blog, let’s look at this Australia’s new biggest city.

As of August 2023, Greater Melbourne’s House Market Pressure is Balanced. With a recovery occurring.

Among the 6 metrics InvestorKit uses to measure market performance, Melbourne’s rental pressure and Growth Cycle both stand out, while rental yield and affordability are the weakest points.

Demographic & Economic Trends

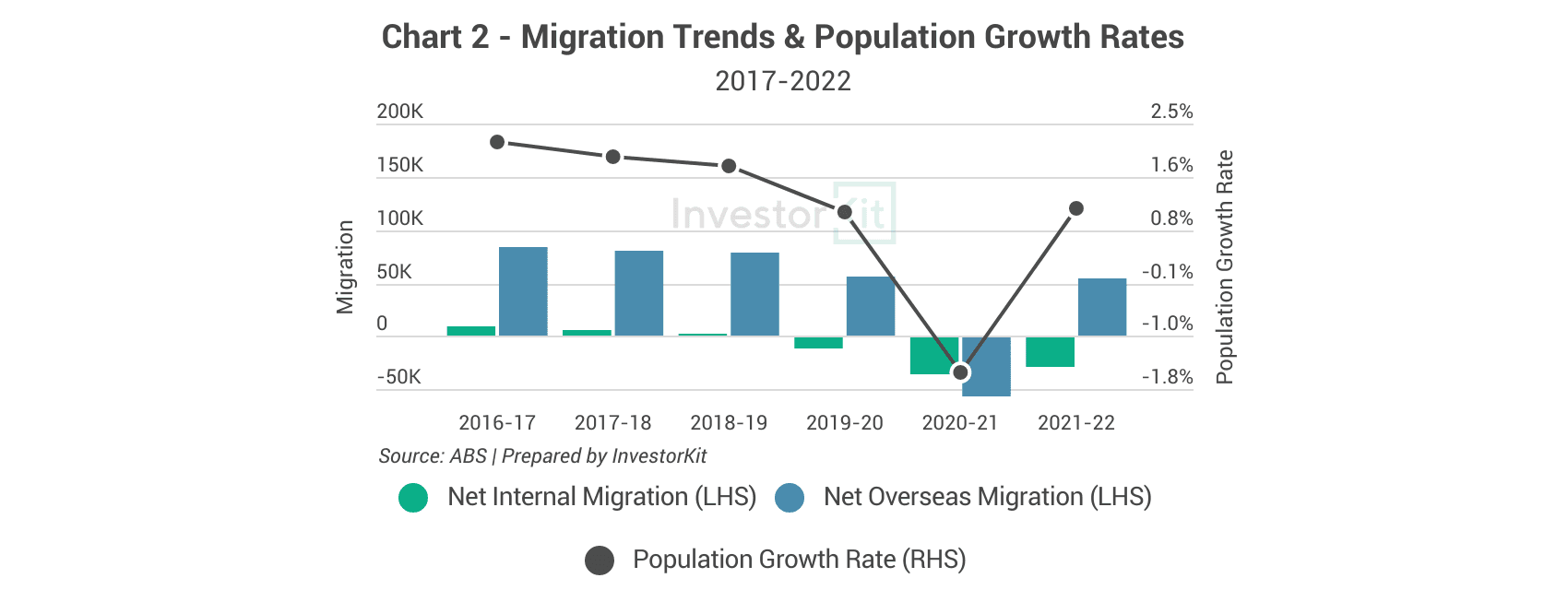

Melbourne’s population growth is quickly picking up strength. In the few years leading to the pandemic, the city’s net internal migration and net overseas migration were both declining, leading to a downward trend in population growth rates. However, as the economy recovers and the affordability advantage (relative to Sydney) becomes more obvious in this high interest rate time, we’re seeing both migration trends bouncing.

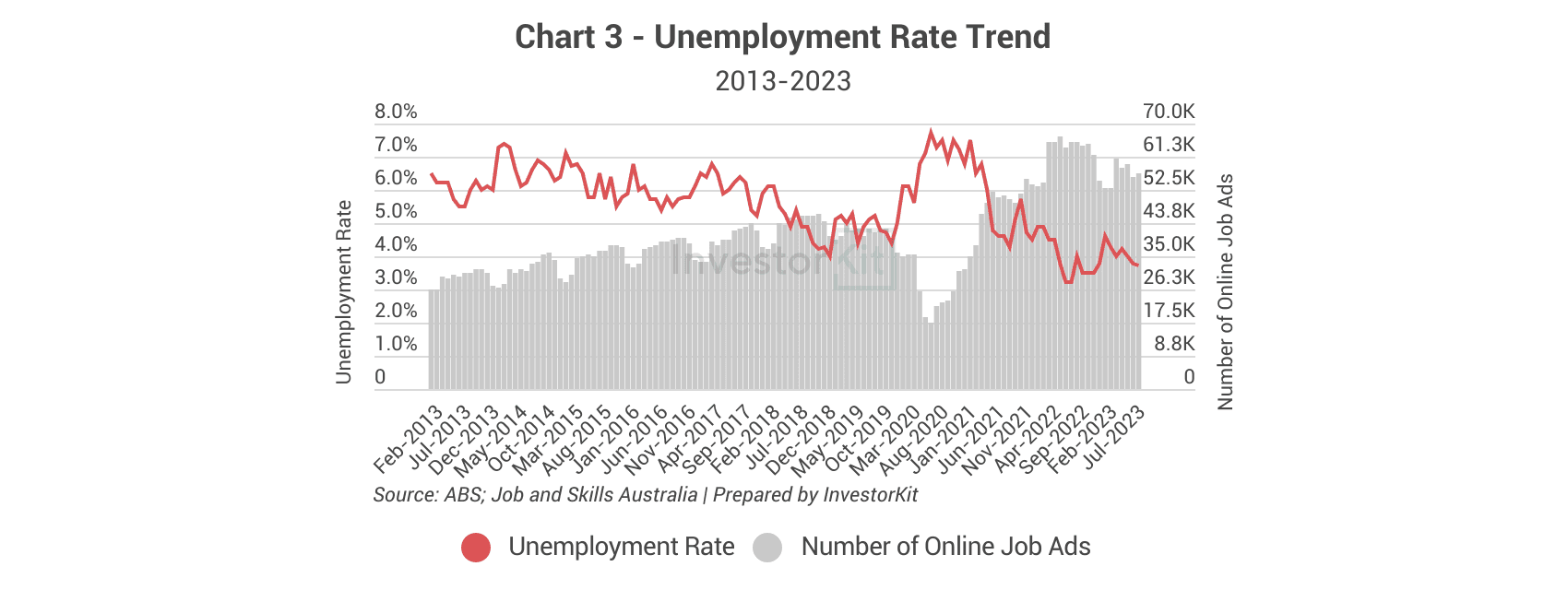

Unemployment rate is hovering around the lowest level in more than a decade, indicating a thriving local economy.

As the RBA cash rate hikes, the total number of job vacancies in Greater Melbourne have been declining slowly over the past year. Unemployment rate is expected to follow this trend to rise gradually in the coming 1-2 years with changing economic winds and rising migration levels.

Sales Market Trends

Greater Melbourne’s median house price has been recovering from the decline, achieving +1.6% QoQ growth, although the recovery is not as fast as the other major cities such as Sydney (+3.8%), Brisbane (+4.2%), Adelaide (+3.4%, Adelaide continues its growth cycle with almost no decline, Perth is the same), and Perth (+2.8%).

The rising sale days on market indicates a release of market pressure; However, it’s expected to stabilise or decline as the market recovers.

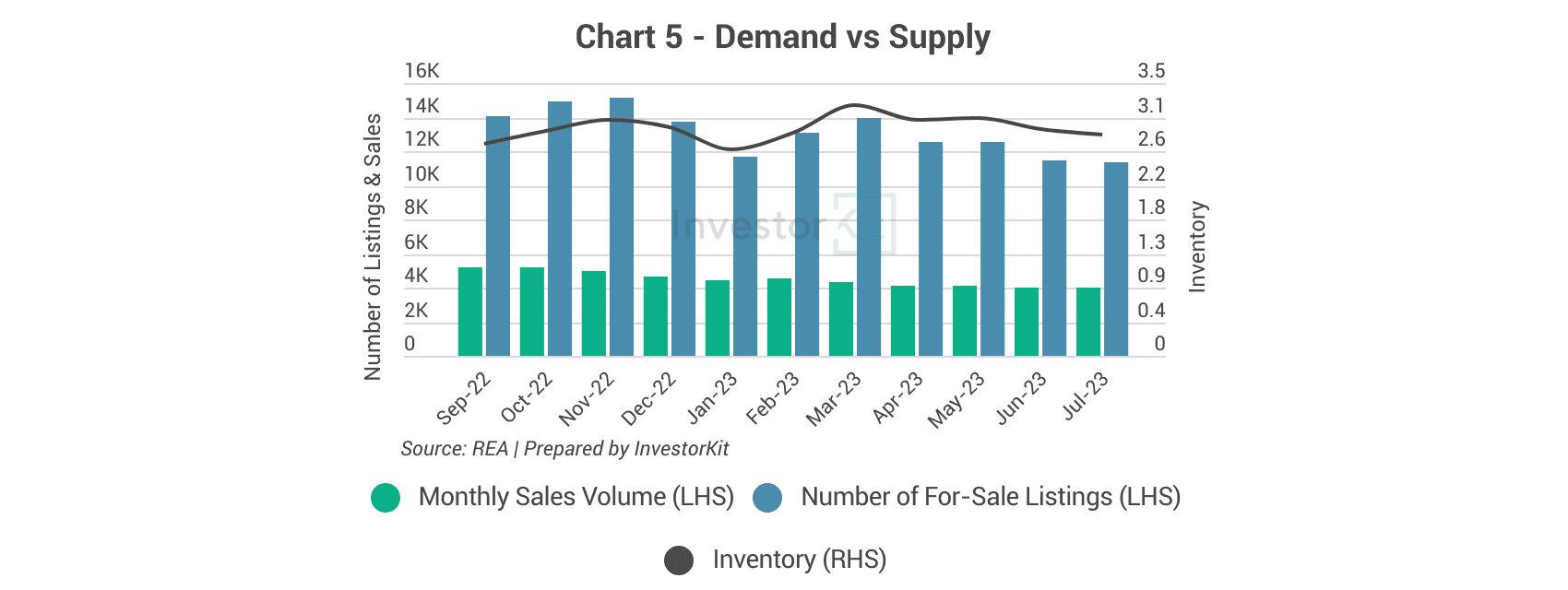

Just like what’s happening in Sydney, Melbourne’s for-sale stock is shrinking fast, which leads to a decline in inventory since early 2023. Again, listing levels vs sales volumes will be key to watch in order to understand how the recovery goes from here.

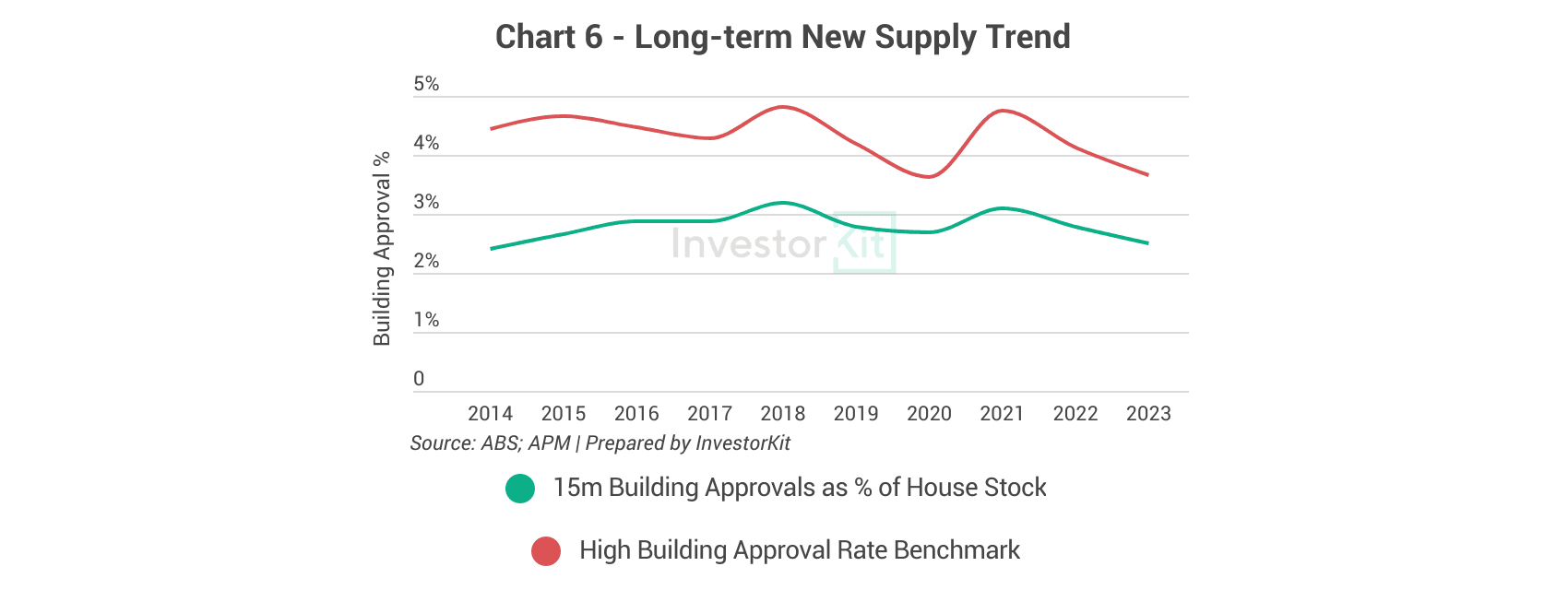

In the past decade, Melbourne’s new house construction activities remained stable at a moderate level compared to its robust population (housing demand) growth. There were periods of oversupply in the decade but like the national trend construction has seen a decline in recent years.

Melbourne’s house price increased by 75.3% in the past 10 years, slightly higher than its long-term average and Capital Cities average. However, in the past 5 years, Melbourne’s performance was substantially behind the Capital Cities average level. This 5-year growth gap is likely to boost Melbourne to start a new wave of growth in the coming years should other recovery trends continue.

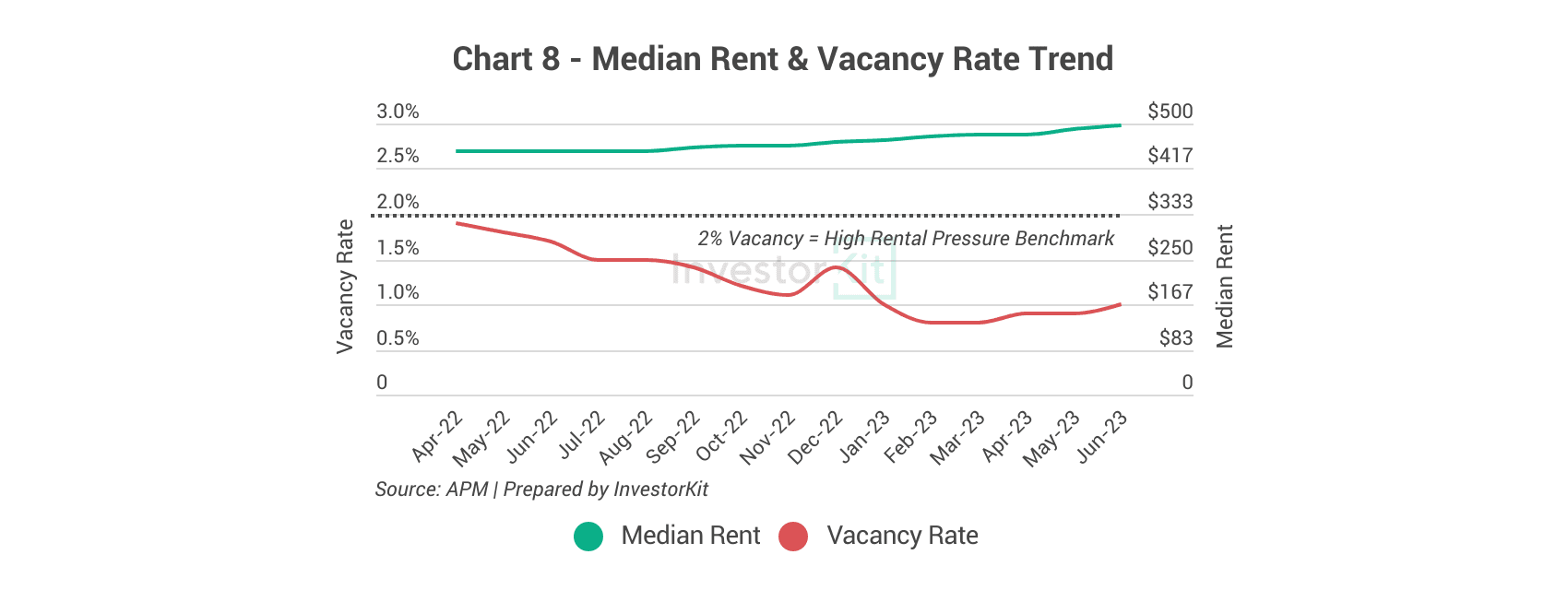

Rental Market Trends

The rental market is under high pressure with around 1.0% vacancy rate. This high pressure has led to a 10.0% annual increase in house rental prices and the highest quarterly house rental growth (3.5%) in the second quarter of 2023. Further increases are expected as Melbourne remains one of the more affordable capital-city rental markets.

The fast rental price growth has contributed to a lift in Greater Melbourne’s rental yield level. However, it is still quite low compared to the smaller capital cities, such as Brisbane, Adelaide and Perth, and the high mortgage interest rates. We expect rental yields in Melbourne to further increase as the strong rental price growth continues. Should interest rates decline which is expected over the next 12 months by many, these recovering yields will become attractive.

Over the past decade, Greater Melbourne’s rental price has grown by 33.8%, in line with greater Captital Cities average growth rate. However, we expect this to increase further considering the robust rental growth momentum and the current low rental price level.

In the next 6-12 months…

Greater Melbourne’s housing market benefits from a strong recovery in both internal and overseas migration trends, an active local economy, and improved confidence evidenced by higher clearance rates than the same time last year. We believe the housing prices in Greater Melbourne will keep growing in the 6-12 months at an improving pace until financial market conditions change and consumer confidence recovers substantially. As the above changes occur, Melbourne could very well move into a stronger phase of a growth cycle and be among the top performers in the 3-5 years ahead considering higher macro housing demand, low supply, and relatively low growth in the past 5 years. Over the next 6-12 months conditions are improving, however, various other capitals will likely perform to a higher level.

Melbourne is the second city we examine in this Market Pressure Review Blog Series. Stay tuned for more cities to follow! InvestorKit is a data-driven buyers’ agency that chooses purchasing locations through a sophisticated market pressure analysis system. This methodology has enabled our clients to achieve growth higher than the average and expedite their investment journey. Interested in learning more about InvestorKit’s research and services? Talk to us today by clicking here and requesting your 45-min FREE no-obligation consultation!

Keep Reading

" transform="translate(5 5)" width="14px"/></svg>)